Austin Lease Market: Record Supply, Softer Rents, Clear Leverage Shift

Tenants have the upper hand. Active rentals in October hit a new high for the Austin area, while median rent has fallen from $2,299 in July 2023 to $2,050 in October 2025, a 10.83% decline. That combination—more choice and lower pricing—defines today’s austin real estate landscape for leases.

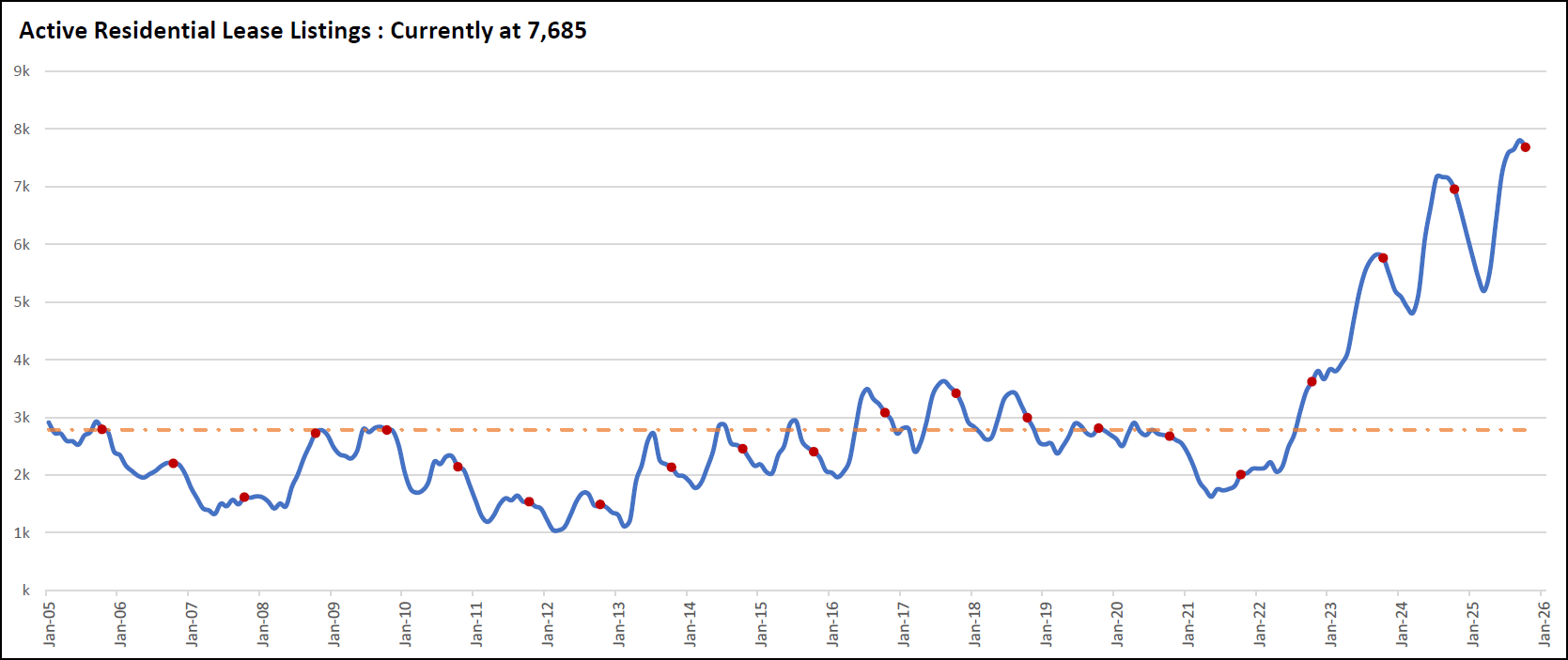

The surge in supply is unmistakable. October closed with 7,685 active residential lease listings across the Austin area, the highest monthly reading in the data series back to 2005. A year ago, October stood at 6,957; two years ago, it was 3,619. The long view matters: pre-pandemic “normal” was closer to 2,000–3,000 active listings. Today’s figure is not a blip; it’s a structural shift driven by new deliveries, investor-owned units returning to market, and slower absorption.

Pricing reflects that pressure. Since the July 2023 peak, median rent has eased 10.83% to $2,050 as of October 2025. That reset is restoring affordability and options for tenants without collapsing the austin property market. It’s also forcing landlords to compete on presentation, price, and concessions. In practical terms, well-located properties still lease, but the market no longer rewards “stretch” list prices.

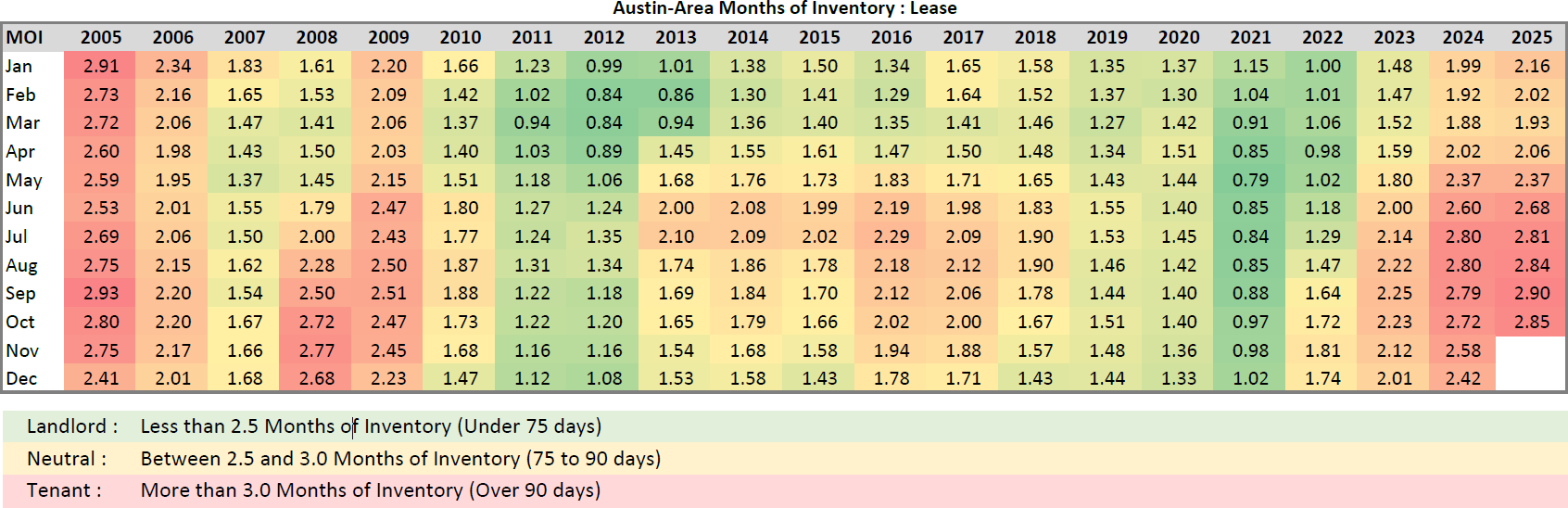

Months of Inventory (MOI) confirms the leverage shift. October’s lease MOI printed at 2.85, up from 2.72 last October and far above the 0.79 trough in May 2021. In this framework, sub-2.5 months favors landlords, 2.5–3.0 is neutral, and above 3.0 tilts tenant-friendly. At 2.85, Austin sits in a neutral-to-tenant zone with a clear lean toward renters given the record active supply. That context matters: we’re near the highest MOI readings in the 20-year record, signaling a market where tenants can be selective and negotiate.

Seasonality is present but not dominant. Active supply eased slightly from September’s 7,802 to October’s 7,685, a typical fall drift. Yet YoY supply growth remains strong (+10.5%), and MOI rose YoY, underscoring that today’s austin housing trends are being driven by higher baseline inventory, not just seasonality. For tenants, the strategy is straightforward: widen the search radius, compare like-for-like options, and use days-on-market to press for value. For landlords, “price to the market you have, not the market you remember” is the winning tactic.

What this means for each group is direct. Tenants should treat list prices as starting points and ask for concessions like pro-rated move-ins or minor improvements. Landlords should identify the true comp set at today’s absorption, not last spring’s, and front-load value with cleaner presentation and responsive terms. Investors should view the current environment as a spread opportunity: soft purchase pricing plus stabilized, cash-flow-oriented rents, with upside tied to demand normalization over a multi-year horizon. None of this is speculative; the record supply, the higher MOI, and the 10.83% rent pullback frame the next several quarters for the austin real estate market.

The path forward hinges on absorption. If active listings hold near present levels into winter while new leasing demand slows, expect further normalization in asking rents and continued emphasis on concessions. If absorption firms in Q1 with job growth and in-migration, MOI can stabilize near neutral and cap additional price softness. Either way, the strategy is data-first: track MOI, watch YoY active supply, and align pricing to the current comp band rather than the peak period.

In short, the Austin lease market has reset. Supply is at a record, MOI sits in neutral-to-tenant territory, and median rent is down meaningfully from the peak. The austin housing market for leases now rewards precision: accurate pricing for landlords, patient comparison for tenants, and disciplined underwriting for investors. Agents who anchor advice to these numbers will win client trust—and better outcomes—through the cycle.

FAQ

What is driving record-high active lease inventory in Austin?

A combination of new construction deliveries, investor units rotating back to long-term rental, and slower absorption has pushed active listings to 7,685 in October—the highest in the series since 2005. That scale of supply materially increases tenant choice across submarkets.

Are rents falling across the board or only in certain areas?

Market-wide median rent has declined from $2,299 (July 2023) to $2,050 (October 2025), down 10.83%. The pullback is broad, though the depth varies by product age, location, and amenities. Newer, amenity-rich assets tend to hold better; older stock and higher-priced outliers face the most pressure.

How does Months of Inventory (MOI) translate to negotiating power?

MOI near 3.0 signals balanced-to-tenant conditions. October’s 2.85 versus last year’s 2.72 confirms leverage has tilted toward renters. In practice, tenants can negotiate on price, timing, or small improvements; landlords win by meeting the market early with clean pricing and presentation.

Is this just seasonal, or a structural change in the austin real estate market?

There is a seasonal component, but the dominant story is structural: active supply is up 10.5% year over year in October and far above pre-pandemic norms. That sustained elevation in inventory, paired with softer rents, points to a longer normalization period rather than a brief seasonal blip.

What are the smart moves for landlords and investors right now?

Landlords should set pricing off today’s most competitive comps and emphasize speed-to-lease with strong presentation and fair terms. Investors should target assets where entry cap rates and stabilized rents pencil under conservative assumptions, using the current supply to negotiate favorable purchases and terms.