Austin Housing Market 2025: Inventory Up 714% as Prices Stabilize

Published | Posted by Dan Price

Austin’s housing market has expanded more than sevenfold since 2022, signaling a dramatic shift from scarcity to balance — but demand remains cautious and price recovery slow.

Market Overview

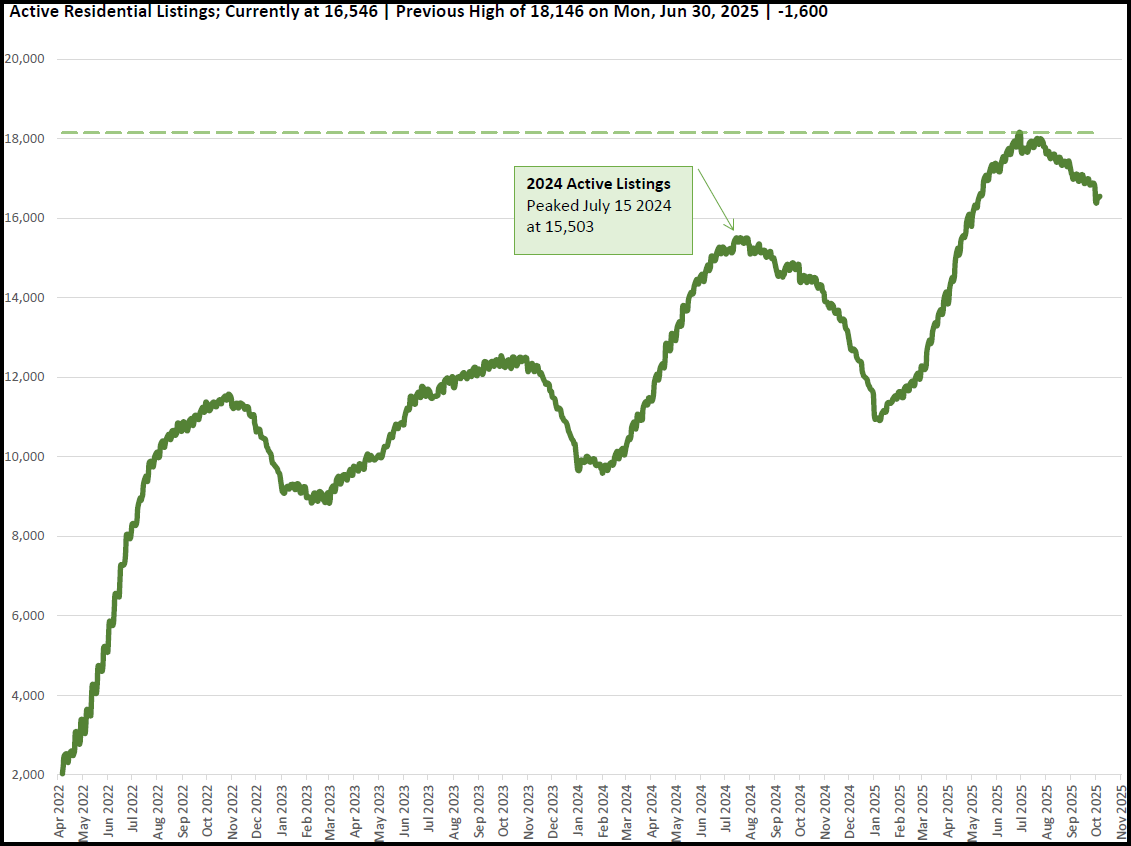

In April 2022, Austin had just 2,031 active listings. Today, that number has surged to 16,546, a 714% increase in only three and a half years. This rebound in supply reflects how the Austin real estate market has transitioned from the feverish shortages of the pandemic era to a far more normalized, data-driven environment. Compared to last year’s 14,554 active listings, inventory is up 13.7% year-over-year, continuing a steady trend of expansion. Nearly 59% of all listings have seen at least one price drop, underscoring the pressure on sellers to stay competitive.

Pending listings tell a different story. At 3,795, pendings are down 5.6% YoY, with cumulative pendings for 2025 now 9.4% below 2024. That combination — rising inventory and fewer accepted contracts — pushes the Activity Index down to 18.7%, compared with 21.6% a year ago. In simpler terms, buyers have regained control of the tempo, and homes are moving more slowly.

Housing Prices and Market Cycles

Prices remain well off their 2022 peaks but show early signs of stabilization. The average sold price for September closed at $550,131, a $132,000 (-19.3%) decline from the May 2022 high of $681,939. The median sold price sits at $417,500, still 24.1% (-$133,000) below its all-time peak.

Austin’s long-term performance, however, tells a different story. The market’s 25-year compound appreciation rate is 4.666%, which means that if $417,500 represents the post-correction bottom, Austin would likely return to its prior peak around December 2031. That’s roughly 76 months away — a recovery period consistent with other major U.S. metros that have experienced post-boom corrections.

The steep inventory increase from 2,031 to 16,546 has effectively reset pricing leverage. Buyers who were once outbid in 2021 now face one of the most negotiable markets in two decades.

Inventory and Market Efficiency

Austin’s Months of Inventory (MOI) has climbed from 5.19 in 2024 to 5.86 today, a 12.9% increase year over year. Historically, Austin’s neutral zone sits near 4.5 months, meaning today’s market carries roughly 30% more supply than a balanced level.

The Absorption Rate — the share of listings that sell in a given period — now reads 17.1%, compared to the long-term average of 31.8%. This sharp drop confirms that while supply has surged, demand hasn’t matched pace. The Market Flow Score (MFS), Team Price Real Estate’s proprietary turnover index, registers 5.44, below the historical mean of 6.59, indicating slower market velocity and longer time on market for most listings.

Segmentation and Regional Variations

Not every price tier or city behaves the same. The bottom 25th percentile of homes saw prices fall 2.9% YoY, while the top 25th percentile gained 2.8%, proving that higher-end segments are stabilizing faster. Out of 29 tracked cities, nine recorded price appreciation, while 20 remained down.

Markets such as Leander, Georgetown, and Liberty Hill continue to see active new-construction pipelines that keep supply elevated. Austin proper, Buda, and Pflugerville, by contrast, show smaller swings, suggesting localized equilibrium. This unevenness is characteristic of mid-cycle markets where affordability bands and builder incentives heavily influence demand.

New Construction vs. Resale

New construction now represents 24.7% of pending contracts, compared with 16.3% for resale. Builders maintain an edge by offering mortgage rate buydowns, price incentives, and move-in-ready inventory. This continues to undercut resale sellers in the $350K–$500K range — where monthly payments often look similar across new and existing homes.

For traditional sellers, this means pricing precision matters. With nearly 60% of all listings having already reduced price, entering the market at or near comparable sale levels is critical. Overpricing by even 2–3% can result in weeks of lost momentum and increased carrying costs.

Transaction Volume and Agent Productivity

Through September 2025, the Austin area has closed 23,094 residential sales, down 3.4% YoY but still 6.4% above the historical average. Adjusted for population, the sales-per-capita rate (903 per 100,000 residents) remains 21.5% below average, meaning growth in population has outpaced transaction volume.

For agents, that means the market rewards precision over volume. The number of sales per 1,000 Realtors rose 0.9% this year — a small but telling sign that active, data-driven agents are capturing market share as less-productive agents exit the field.

Outlook and Forecast

Austin’s current trajectory aligns with a classic mid-cycle correction. Supply continues to build, demand has flattened, and prices have likely found their post-boom equilibrium. With 16,546 active listings, up 714% from 2022, the structural inventory problem that once defined the pandemic market has been resolved — perhaps over-resolved.

Looking ahead, recovery hinges on three key factors:

Interest Rates: Stability below 6.5% would improve affordability and pull pent-up buyers back into play.

Employment Growth: Austin’s diversified job base remains a buffer against national slowdowns.

Migration Patterns: Continued in-migration from higher-cost states should sustain long-term demand, though less aggressively than in 2020–2021.

The likely outcome: a steady, gradual re-acceleration beginning in late 2026 — a market driven by fundamentals rather than frenzy.

For Buyers, Sellers, and Investors

For buyers, this is the most flexible environment in years. More listings, longer DOM, and widespread price adjustments translate into meaningful negotiating power. For sellers, precision is everything. Pricing to the data — not to sentiment — determines whether a home sells or stagnates. For investors, yields have improved materially. With median prices still 24% below peak and cap rates moving above 6%, Austin’s rental math once again makes sense for cash-flow buyers targeting submarkets like Hutto, Kyle, and Leander.

Conclusion

The Austin housing market has come full circle — from record scarcity in 2022 to measured abundance in 2025. The seven-fold jump in inventory underscores how dramatically conditions have changed. Yet through the noise, Austin remains resilient: prices are stable, employment is strong, and migration keeps the long-term outlook positive.

What we’re witnessing is not collapse but recalibration — a patient return to fundamentals that will define Austin’s next housing cycle.

FAQ Section

1. Why has Austin’s housing inventory risen so sharply since 2022?

Active listings climbed from 2,031 in April 2022 to 16,546 today — a 714% increase. Builders caught up with demand while higher mortgage rates slowed new buyers. The result is a balanced market rather than the undersupplied chaos of 2021.

2. Are Austin home prices still falling in 2025?

No, the major correction has already occurred. Median prices stabilized around $417,500 after a 24% drop from 2022 peaks. Month-to-month volatility remains mild, suggesting a base has formed.

3. Is this a good time to buy in the Austin area?

For long-term buyers, yes. Abundant supply and motivated sellers create opportunity. With nearly 60% of active listings having cut prices, well-qualified buyers can negotiate favorable terms before rates decline and competition returns.

4. How do today’s market conditions compare to the 2008 downturn?

Austin’s fundamentals are much stronger. Job growth, tech employment, and migration are all positive. The current slowdown stems from affordability and rate pressure — not distress — making it a cyclical correction rather than a structural collapse.

5. When will Austin home prices return to their 2022 highs?

Based on a 4.666% compound appreciation rate, Austin’s median price could recover to $550,000 around December 2031. That seven-year climb is typical for maturing markets following rapid booms.

Related Articles

Keep reading other bits of knowledge from our team.

Request Info

Have a question about this article or want to learn more?