Austin Real Estate Market Overview

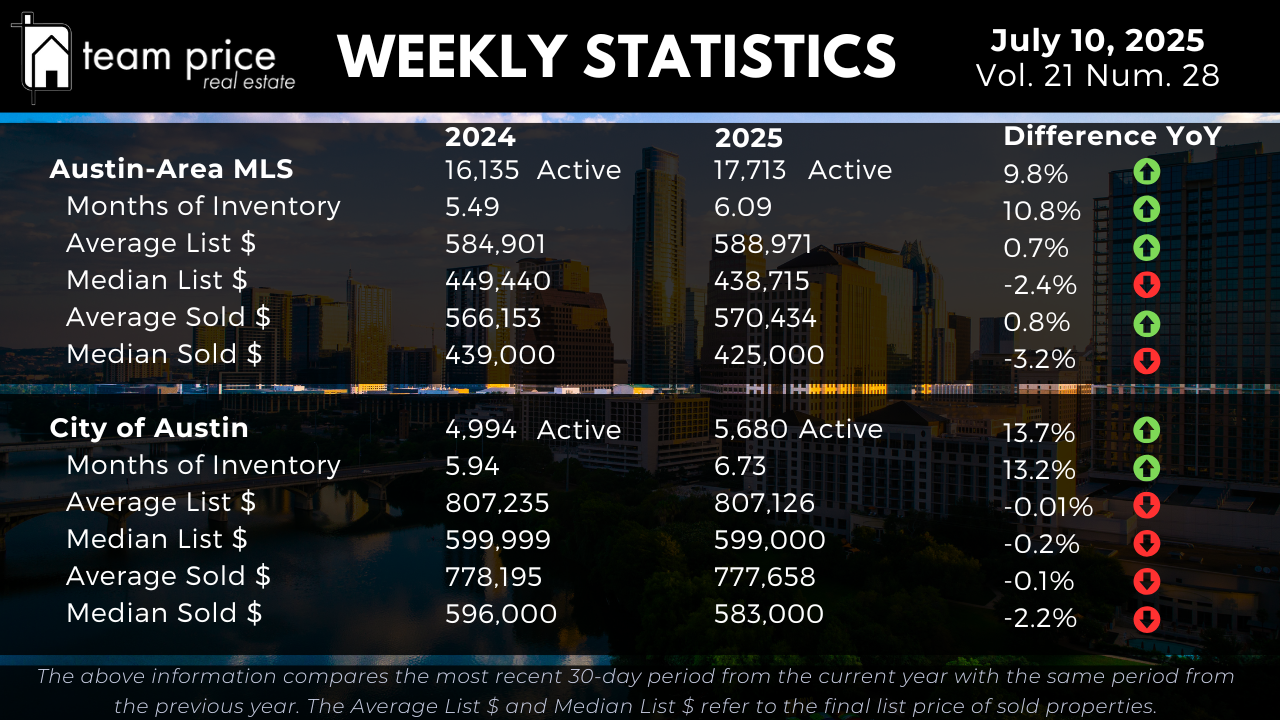

Inventory levels across the Austin-Area MLS continue to climb steadily, reinforcing that the region remains in a prolonged transition phase. As of this week, there are 17,713 active residential listings, representing a 9.8% year-over-year increase. Months of Inventory has expanded to 6.09, up from 5.49 a year ago—a 10.8% gain that reflects a market where supply is growing faster than demand. Within the City of Austin, this trend is even more pronounced. Active listings are up 13.7%, now at 5,680 homes, while Months of Inventory has risen to 6.73 from 5.94 last year—an increase of 13.2%. The continued growth in available homes gives buyers more leverage, greater negotiating power, and an increasing ability to wait for the right opportunity.

Austin Housing Prices: Stability with Pockets of Softness

The latest pricing data illustrates a market attempting to balance between softening demand and seller expectations. Across the Austin-Area MLS, the average list price of active homes is $588,971—up just 0.70% year over year—while the median list price has dropped by 2.39% to $438,715. On the sales side, the average sold price has nudged up 0.8% from last year to $570,434, while the median sold price declined 3.2% to $425,000. These figures indicate that while higher-end sales are helping stabilize average prices, affordability concerns and greater competition are compressing the mid-tier and entry-level segments.

Within the City of Austin, pricing trends reflect even more stagnation. The average list price has held flat year over year at $807,126, showing virtually no movement. The median list price dipped marginally by 0.2% to $599,000. Meanwhile, the average sold price decreased slightly by 0.1% to $777,658, and the median sold price declined 2.2% to $583,000. The data suggests that sellers, particularly those in the $550,000 to $650,000 range, must now compete more aggressively as pricing continues to drift and buyers remain cautious in response to rate sensitivity and expanded choices.

Regional Trends: Correction Persists Across Central Texas

Conditions across the broader Central Texas region continue to reflect a market correction rather than recovery. Among the 30 cities monitored, just 33% (10 cities) posted month-over-month price increases, while 60% saw declines. Year over year, only 10 out of 30 cities have experienced price gains—just 33%—while the remaining 67% have declined. Notably, none of these cities have surpassed their price peak from the past 12 months, reinforcing that while some localized momentum exists, the region remains in an extended correction cycle.

The ZIP code data mirrors this broader trend. Of the 75 ZIP codes tracked, 48% showed month-over-month price gains, while 48% recorded declines—indicating a near-even split with no clear directional trend. On a year-over-year basis, 36 ZIP codes have posted price increases (48%), while 39 have declined (52%). Only 4 ZIP codes are currently above their 12-month pricing peaks, a clear sign that most submarkets remain in a rebalancing phase, with few having fully recovered to prior highs.

List-to-Sale Price Performance: Negotiation Remains the Norm

The prevalence of price negotiation continues to define this market cycle. So far this month, 67.74% of all sold homes in the Austin-Area MLS have closed below their original list price—up from 65.92% the previous month. An additional 21.24% of sales closed exactly at asking price, while only 11.02% sold above list, down from 12.25% in June and 13.22% in July of last year. The average sold-to-list price ratio currently sits at 97.27%, confirming that modest seller concessions are now routine. This data underscores the importance of precision pricing and strong presentation, especially as buyers are growing more strategic and inventory continues to build.

Peak Value Trends: Market Remains Well Below Previous Highs

While recent pricing has shown relative steadiness, the broader market remains significantly below its prior peaks. In the Austin-Area MLS, the average list price reached a high of $714,434 in April 2025 and has since declined to $635,914—a drop of 10.9%. The median list price peaked at $539,900 in May 2022 and is now down 14.9% to $459,000. The average sold price has fallen 10.6% from its May 2022 high of $664,515 to $594,371, while the median sold price is down 18.2%, from $538,000 to $440,000. Price per square foot trends show similar declines: the average dropped 19.1% from $324 to $262, and the median fell 23.2% from $280 to $215.

The City of Austin follows this same trend. The average list price hit $948,840 in April 2025 and now stands at $840,651, down 11.4%. The median list price is down 11.3%, from $659,500 to $585,000. The average sold price has declined 8.1% from its peak of $847,583 to $779,230, while the median sold price has dropped 17.3% from $680,000 to $562,500. The average price per square foot has decreased by 21.9%, from $442 to $345, and the median has fallen 21.9%, from $393 to $307. These metrics confirm that although the market is showing signs of finding balance, it remains well below its peak values—underscoring the extended nature of the correction and the need for informed decision-making in today’s environment.