Austin Housing TOP Questions and Answers

What is the latest update on the Austin housing market?

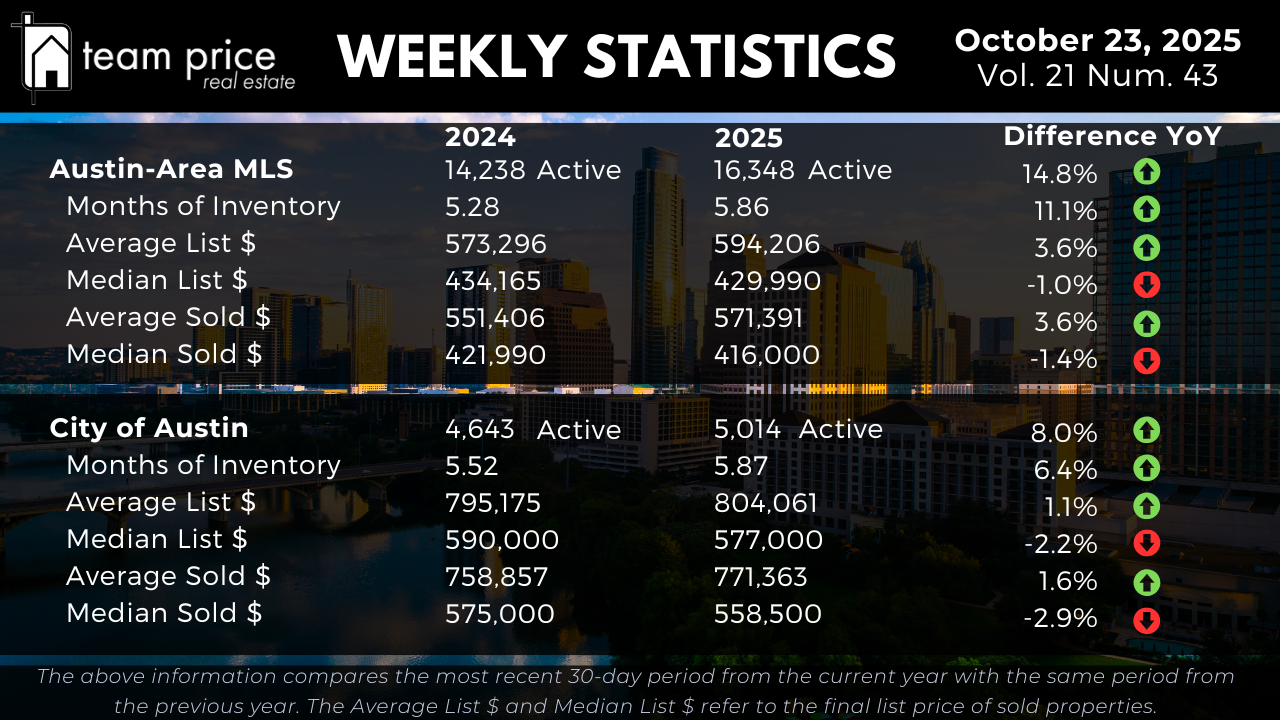

The Austin housing market is in a clear phase of rebalancing as inventory continues to rise and buyer absorption slows. Active listings across the Austin-Area MLS have increased 14.8% year over year, from 14,238 to 16,348, while Months of Inventory has climbed from 5.28 to 5.86—a rise of 11.1%. Within the City of Austin, inventory has grown 8.0%, and Months of Inventory has increased from 5.52 to 5.87. This expansion in supply confirms that homes are taking longer to sell, and the market is transitioning toward a more buyer-favorable environment.

Are home prices in Austin dropping?

Median prices are experiencing moderate declines year over year, indicating downward movement in typical buyer segments. Across the Austin-Area MLS, the median sold price declined 1.4%, from $421,990 to $416,000. In the City of Austin, the median sold price fell 2.9%, from $575,000 to $558,500. Median list prices are also down, with the Austin-Area MLS recording a 1.0% decrease and the City of Austin showing a 2.2% decline. While average prices are slightly up due to higher-end transactions, the median figures reflect softening in the core market.

What is the real estate market in Austin in 2025?

The 2025 market is defined by increased inventory, slower absorption, and pricing that is stable at the average level but declining at the median level. Active listings are up across both the metro and the city, and Months of Inventory has risen, indicating reduced urgency among buyers. The average sold price in the Austin-Area MLS is up 3.6%, but the median sold price is down 1.4%, showing a shift toward affordability and negotiation-driven transactions. The market is no longer in a rapid growth phase but is operating in a state of normalization.

Is Austin's boom over?

Based solely on the data, the boom phase has concluded, and the market is now in a post-peak normalization cycle. From their 12-month peak, all 30 tracked cities and 74 of 75 ZIP codes have seen prices decline. Months of Inventory has increased across the metro and the city, signaling a transition from rapid expansion to a balanced or supply-heavy market environment. Prices are no longer accelerating; instead, they have settled into a stable but softened range compared to peak conditions.

Is it better to buy a house now or wait until 2025?

Based strictly on current conditions, 2025 is already underway, and the data reflects that buyers currently have increased leverage. With 69.21% of homes selling below list price and the average sold-to-list ratio at 96.95%, buyers are negotiating meaningful discounts. Inventory is at its highest level in recent years, and most ZIP codes are trading below their peak values. The current environment favors buyers more than sellers, indicating that conditions are advantageous now rather than improving later.

Is Austin a buyers or sellers market?

Austin is trending firmly toward a buyer’s market. Months of Inventory across the Austin-Area MLS has risen to 5.86 months, and in the City of Austin it is now 5.87 months—both above the traditional threshold of five months that marks the beginning of buyer-favorable conditions. Additionally, nearly seven out of ten homes are selling under list price, while only 12.38% are selling above list. These figures indicate that buyers have leverage in negotiations, and sellers must compete more aggressively on price.